Liquidity Farming is harmful for Public Goods

Liquidity Farming is harmful for Public Goods

About the dangers of using Liquidity Farming DAOs for funding Social Impact projects, due to flawed incentives and the distortion of price signals.

Where is the Intrinsic Value?

Public Goods funding has been the most challenging problem that the blockchain industry has attempted to solve, while many projects hope to tackle this with innovative market engineering built on top of smart-contracts logic. The clue is learning how to offer economic incentives to investors for contributing to public goods development, despite these kinds of projects cannot be self-sustained by the means of trade.

Due to the market failures in public goods development, these assets are prone to be abused by "free-riders" to the detriment of those who contribute with their effort and resources for maintaining them. For that reason, blockchain entrepreneurs have been motivated to develop coordination games through experimental economic models, mostly based on creating artificial value represented in the form of digital tokens that reward participants.

Inspired by DeFi solutions like Uniswap or Bancor, many solutions have developed a kind of DAO platform that collects liquid assets for funding social impact projects and yields artificial DAO tokens in exchange for capital contribution. Typically, is expected that such DAO tokens would have some intrinsic value for investors, either for governance voting or community oriented activities. The prevalent business model in all these platforms is that investors would obtain benefits by serving as liquidity providers in secondary markets, as they generate ROI by selling those community tokens that they've acquired early at a discounted price.

The first problem that these solutions face is precisely the lack of intrinsic value that the DAO token represents. And in consequence, investors often feel the urgency of recovering the liquid capital that they have staked in the DAO treasury.

Social Impact solutions mostly derived from the developments of Commons Stack initiative, like Giveth, Radicle, and DEV employ Token Engineering strategies for preventing investors from redeeming their community tokens and pulling back the liquidity from the pooled funds. And in compensation to the investors, they would offer either staking rewards or price arbitration opportunities for making a profit.

Putting away the altruistic intentions for funding social causes, Social Impact DAOs have to compete with other commercial-oriented DeFi platforms in order to attract investors on board on their projects. These investors would prefer to park their liquid capital where it yields more profit, thus they would choose the commercial-oriented alternatives as they offer optimal capital efficiency.

Because of the requirement to reserve a good chunk of liquid capital for funding public goods causes, social impact projects tend to perform poorly, thus ending up displaying low capital efficiency. At the same time, these DAOs must preserve a portion of that liquid capital for granting investors redeeming their community tokens under certain conditions. This could potentially create a conflict of interests when serving both objectives at the same time.

So we often see vesting policies in Social Impact DAOs, for not allowing the immediate conversion of the staked tokens to liquid capital from the pool. Many users complain that the procedure for redeeming those tokens is quite confusing, and requires approval from an authority that studies each case. Therefore, the chances that investors have for exiting the DAO pool are few.

In contrast, commercial-oriented DeFi solutions like Bancor always guarantee the redemption of DAO tokens into their equivalent liquid capital from their treasury, and this only could be done when the platform ensures a good provision of a diverse basket of liquid tokens that can be exchanged within the Bancor platform.

As the liquidity options are severely limited in these Social Impact DAOs, their only way to reward investors is with governance or community tokens. However, those tokens don't have a clear utility beyond the democratic participation in projects (and perhaps in deciding how to expend the collected treasure).

So they resort to minting new DAO tokens just for rewarding long-term holders that staking them, driving thru inflationary pressures with the risk of losing value from the invested capital. Additionally, those platforms deny the redemption of DAO tokens because there isn't just enough collateral in the treasure for backing them.

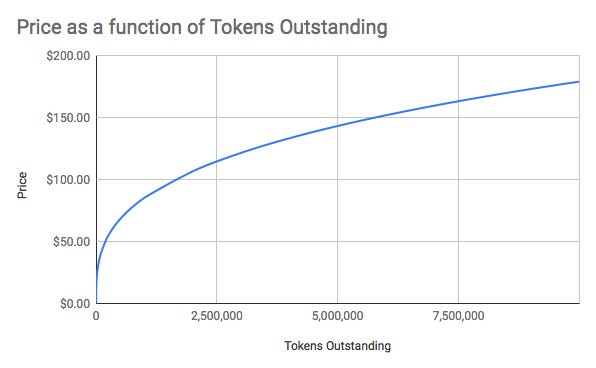

Then, the other approach for encouraging investors is propping the value of DAO tokens algorithmically with a Smart Contract that allows emitting tokens continuously by demand and adjusting the price dynamically to a Bonding Curve function. This innovation was first introduced by Simon de la Rouviere when he formulated a price discovery system for curation markets, from which the basic idea is letting the community decide which content deserves to be encouraged and preserved by staking tokens on the selected data channels.

Simon de la Rouviere believed that free market dynamics cannot bestow a proper price to information resources in data markets. Because of the lack of price signals, it just requires configuring a coordination game between agents to drive the demand artificially. These agents could raise the price when interacting with the bonding curve system and buy more tokens, or lowering the price when they burn their tokens and redeem the equivalent collateral asset held in the treasure.

In that way, agents would look for price arbitration opportunities when they buy earlier at a discounted price. Eventually, they would be selling those tokens in later stages when the price is higher and obtaining profit from the difference. As the price is dictated by an algorithm that supposedly reduces the speculative risks, it helps agents predict the expected returns deterministically.

Coordination Failure caused by Wrong Incentives

By configuring a Bonding Curve with a sublinear logarithmic function, Simon de la Rouviere proposes a method for rewarding early adopters as they're looking to buy the tokens from a project as soon as possible, while the least interested would have to pay more when entry later in the economic game. Simon de la Rouviere believes that rewarding early adopters in that way would help crowdfunding campaigns, leading to a FOMO rally that encourages frenetic participation from investors.

This idea has been practically implemented by some projects that demonstrated the effectiveness of this strategy for raising funds. The Ocean Protocol, IdeaMarket, and Jucicebox DAO hosted many successful funding campaigns as many looked for opportunities for generating profit in the process.

However, nobody could predict the negative consequences carried by the wrong incentives that this economic game introduces.

What actually happened is that investors were just chasing liquid treasury resources and taking advantage of others by exploiting the algorithm: some got the upper hand by paying more transaction gas fees, thus they would get more tokens sooner than other competitors.

In addition, the project organizers could extract a large part of the treasury funds at the right time when the price is optimal, since they may have obtained a large supply of tokens for themselves in the early stages. This type of scam is known as a "Rug-Pull" scheme, and it has occurred very frequently in the history of operations of these DAO platforms, raising questions about the integrity and ethics of the proposed solution.

Even so, many Bonding Curve DAO projects do not really care about the social impact of their funding campaigns, due to the obvious disconnection between the economic game and the commitment of the proposed social goals. Investors only look for price signals driven by the algorithm, but not on the execution of the development of the public good performed by the organizers. And those bad incentives lead some privileged actors to deceive unaware investors with false promises of high returns.

Due to the alarming rate of fraudulent cases in Ocean Protocol, initiatives like Rugpull Index have been developed with the sole purpose of informing the public about the risk profile for the projects in the platform. Those rug-pull cases are already listed on this website available for everyone. Its author, Tim Daubenschütz, developed a decentralized scoring mechanism for detecting when malicious users create their own liquidity pool with an automated market maker (AAM) and then lures other liquidity providers or buyers/sellers into using the pool.

The findings discovered by Tim Daubenschütz reveal the misalignment between the economic motivations from investors and the quality development from the data providers. The relevance of information from data channels doesn't matter at all, as long as data pools gather a huge number of investors that contribute with liquid capital in the treasury. Thus, the incentive will be always extracting capital from it, instead of helping with knowledge consolidation.

In short, Tim Daubenschütz identified these 5 great problems with the curation markets based on Bonding Curve:

Rug-Pull risk: In Ocean markets, a rugpull is when the owner of a data set intentionally devalues its data token in an attempt to acquire more OCEAN. This can be achieved by minting a lot more data tokens and decreasing the data token’s value in OCEAN terms, or selling the many data tokens they own in return for acquiring more OCEAN. RugpullIndex website is able to detect the degree of concentration of data tokens in hosted projects, indicating the probability that a potential rug-pull scheme could be devised.

Impermanent Loss risk: Impermanent loss can be described as the difference between what you would get if you only held an asset versus acting as a liquidity provider for that asset. Since the main motivation of data investors is simply to extract liquidity from the data pool, the risk of Impermanent loss is high in most cases, leading to a permanent imbalance of liquidity pools where the amount of data tokens data emitted greatly exceeds the deposited liquid capital.

Lack of value proposition from content: Data providers' biggest problem is that they can't make a good value proposition to data consumers. Data consumers always face the risk of buying a rug pull in disguise. It is difficult to understand if a single sale can make a data set worthless.

Staking rewards are more important: OceanDAO members are mostly concerned about the OCEANs that they hold. Their interest is less in the survival of individual projects and more in the correct strategic functioning of the OceanDAO’s funding mechanism. Their ultimate goal is to make a return on their initial OCEAN investment.

Content Quality doesn't matter at all: Since investors in Data Pools are more motivated by the speculation games and price arbitration opportunities, what really matters for them is gathering a large number of investors in the organization. Popularity surpasses quality efforts, as the number of participants is the only factor that affects the price of the tokens. The accuracy of the information doesn't have any effect on the economic game, and cases of stolen data and corruption are very frequent on the platform.

If flawed incentives permeated curation markets where supposedly there is a trading demand for data sources (and people willing to pay for it), what would happen if this model is applied to public goods funding? What makes Digital Public Goods troublesome for commerce activities, is that they can be copied without restrictions. Once they've been created and published to be distributed online, users could produce many copies from them indefinitely at zero cost and never pay for their consumption, driving to a market failure.

Bonding Curve games for funding digital public goods only would remark the already mentioned vicious tendencies, as the economic benefit for investors doesn't have any connection with the project performance. Juicebox DAO aimed to collect funds for these kind of non-commercial projects, by configuring the crowdfunding campaign towards a target funding goal, and that goal will drive the price dynamics through a Bonding Curve token emission.

The premise from Juicebox DAO breaks because of its dependency on the overflowed capital for rewarding investors in crowdfunding campaigns: Simply because at later stages, the motivations from newcomers would decrease when the bonding curve stabilizes to the top-level price (Which means that nobody could take advantage of price arbitration). Therefore, there is a high probability that the target financial goal is never reached so there wouldn't be any excess of capital for paying dividends to early investors.

In synthesis, the kind of practices that lead to coordination failures and negligence on the development of the social impact project are:

Promising future returns without a clear revenue model: As many common pool DAOs, these platforms use the same rhetoric from investment companies generally advertising the APY they will pay for the contributed capital. But probably those returns would come from future investors. Many explain that the provenance of yielded benefits comes from financial adventures in lending platforms, as a form of gambling with other's money.

Reward investors with non-liquid assets: Investors contribute with liquid capital in currencies already accepted by the market. But in exchange, they obtain tokens minted in the DAO.

Price manipulation as the main source of economic benefit: Unable to recognize the true value of the public goods, these kind of DAOs lean towards speculative games as the only source of profit, leading to economic disasters.

Passive investment: Investors trust in the management of funds performed by the administrators of the platform, and expect benefits without taking part in the process.

These practices were conceived from the philosophy of treating Social Impact development as a zero-sum game. This leads to the wrong usage of liquidity farming technologies for funding public goods, which only could produce fraudulent schemes. Very often these DAOs have been cataloged as Ponzi schemes as they share some of their characteristics (F.E. promising future returns for staking funds by relying on contributions from incoming members).

Due to the exposed financial mistakes, initiatives for the usage of blockchain in funding Open Source Software have been backlashed as they've carried a bad reputation. Uninformed developers cannot appreciate the innovations of decentralized finance and smart-contracts, as they've just been observing the abusive practices that have been plagued the ecosystem.

Unable to produce value on their own, current Social Impact DAOs just neglected their mission and also destroyed wealth from their investors. So the question is: Why do many initiatives keep repeating the same mistakes by just adapting the same template of curation markets? As they always rely on Liquidity Farming and Bonding Curve emission.

At last, some researchers have recognized the need for a business logic capable of linking the performance of the financing campaign to the reality of the Social Impact project. That is why Dr. Shruti Appiah proposed the use of Prediction Markets to encourage the aggregation of information about the reality of Social Impact projects.

Maybe, with this aggregated information we could establish an strong link between the social benefit of projects with their market value.

Reputation is the “Alpha” for Intrinsic Value

Appiah's proposal features an "alpha" that helps the algorithm to adjust the price accordingly and penalizes the negligence of the project execution. However, this solution requires honest reporters that provide accurate information about the project through information oracles that feed the system, and this only could be done with the help of an effective Reputation system.

So the question is, which is the most effective system for bestowing reputation to information providers? How to ensure their integrity and making them accountable for the quality of the information? Supposedly Bonding Curve DAOs were created for nurturing quality of information and help providers to build a reputation, but their incentives mechanism depart from that goal.

We need another kind of organization where the quality of digital content establishes a direct relationship with the market value of the digital assets. Then, Reputation should constitute the stronghold of value that supports every relationship in this system. And that is exactly what DAOVOTION is based upon.

The value proposition of DAOVOTION consists of recognizing the true value of Digital Public Goods, as the Reputation that those goods grant to the supporters of Social Impact Projects. This platform remarks the degree of commitment from project developers and supporters, thus ensuring excellence in quality efforts.

In DAOVOTION, Social Impact projects nurture a community of supporters around them. Such community is called Egregore, and those who contribute to an Egregore obtain a membership token which is called Devotee Token. As Devotees from a prestigious Egregore, they develop a Social Capital that serves as Collateral for Information Services, as their liability is based upon the reputation of the Egregore.

The reputation system in DAOVOTION offers unlimited opportunities for prediction markets, as Devotees could perform the role of Jurors and Reporters for attesting the truth about diverse subjects. Indeed, DAOVOTION integrates a system of courts for evaluating the truth about the performance of the projects. Through Arbitration Trials, Egregores prove their Prestige.

Anyway, the revenue for social impact projects doesn't necessarily have to depend on prediction markets or other kinds of financial adventures. In fact, Devotees have an active role in collecting funds for Egregores by selling Devotee Tokens to new members, promoting the project as selling agents.

As the economic activity on Egregores behaves more like a regular commercial business, the selling of memberships (Devotee Tokens) doesn't need to play with price speculations. The entire market could be running entirely on stable coins because prices are fixed on each Egregore by the community consensus.

And the most important aspect is that benefits are paid in stable coins too. That means: if people invest in Dai, their returns will be yielded in Dai.

Thus, the commercial activity performed by Devotees offers enough economic incentives for investors in Egregores. It differentiates from liquidity farming schemes, as Egregores don't have to promise future returns to those investors. Instead, by becoming Devotees, they acknowledge that their benefits will come from their own effort: by performing as sales agents, they do earn commissions for each new membership token that they sell.

| A guest post by

|